☕ Dividends now? Why 8% can cost you 80%

Mar 03, 2026Howdy! 👋

It’s getting spicy.

Futures are down hard in early going as I type, and I expect markets’ll stay that way in contrast to yesterday’s run-up. Ostensibly, traders are coming to terms with the fact that the war in Iran may take longer than expected (as of last night according to US President Donald Trump).

That’s true, but what’s really got traders’ attention is entirely different.

The US 10-Year has jumped to 4.09% which means all that money they’d planned to borrow to juice returns has just gotten a whole lot more expensive. So they’re doing what they always do when this happens… tapping on the brakes and selling in the early going to avoid the institutional equivalent of a big, hairy margin call.

Btw, and if you’re an OBAer, I’ve got a special article in the March issue that’ll explain why (and what to do about it); it publishes Friday if everything goes according to plan and there’s enough coffee in the pantry – so stay tuned! 😀

Meanwhile, remember this.

People think you make your money in bull markets, but the real profits get made when the bears come out to play.

Here’s my playbook.

1 – Time to buy oil?

Many investors are rushing into oil because, well, you know.

Big mistake.

As I noted on Varney & Co yesterday, the time to do that was six months ago for the simple reason that this has been one of the most telegraphed conflicts of all time.

Institutions have been effectively front running this trade for the past month as has the OBA Family. Case in point, my favorite energy choice has returned just a notch over 10% while the S&P 500 has dropped -1.36% over that time frame.

The spread looks to widen this morning with oil trading higher for reasons I’ll get into in a moment.

That’s great for everybody on board but, not coincidentally, a lot like grasping at straws for everybody who isn’t.

If you’re thinking that you’re going to “buy oil” good on ya.

I’m hearing buzz about $100 a barrel and a 70’s style oil shock – which makes me glad that I own a Tesla and Tesla itself, but I digress.

Just do me a favor if you’re gonna buy.

Keep your eyes wide open… oil is a trade at this point and full warning: you’re going to be fighting for Wall Street’s table scraps.

Big difference.

Keith’s Investing Tip: Keith’s Rule of the Back Page applies in spades – meaning that you want to be constantly focused on what’s next. By the time a story hits the front page, it’s old news. The smarter and potentially more profitable course of action is to prepare for what happens when the shooting stops and prices drop.

Speaking of which…

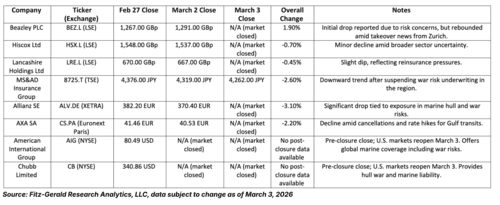

2 – The real oil shock? Lloyd’s said “Nope.”

People think that Hormuz has effectively closed because of all the shooting but that’s only partly true.

The far more critical reason is that insurance companies have stopped providing “War Risk” insurance, and that, in turn, has caused the benchmark freight rate for VLCCs (very large crude carriers) to jump to an all-time high of $423,736 per day according to LSEG.

Let’s put that in context.

We’re talking about a jaw-dropping 94% increase from Friday’s closing rate… and we thought US health insurance companies were bad! 🤦

Speaking of which and also as I suggested would be the case, stock prices for those same insurance companies have dropped since the closure reflecting concerns over potential claims, reinsurance tightening up, and disrupted premiums. (Read)

It’s the same story, different deal.

While it’s true that insurance companies may benefit from surviving coverage, the real risks are outweighed by cancellation and claim fears. At least for now anyway.

Putskies – a bet on declining prices – still pay, at least for now.

3 – Target reminds me of Sears more than ever

Failing retailers always tell some variation of the same story.

Target’s earnings boiled down to this: “yeah, but we’re really poised to end our sales slump”.

Right.

I was born in the middle of night; it just wasn’t last night.

Sales and traffic have picked up but the numbers still stink. (Read)

Net sales came in 1.5% lower YoY for the 2nd quarter in a row.

More than ever, Target reminds me of Sears.

Don’t kid yourself, and buy a retailer that has the numbers, the goods and the management to make owning their stock worthwhile.

Keith’s Investing Tip: This isn’t complicated, but a lot of people make it that way. Buy the best, ignore the rest.®

4 – Japanese companies now own 6% of US market share

Daiwa House and Sekisui – both of which are Japanese homebuilders – purchased two US homebuilders in February. (Read)

- Daiwa House (Stanley Martin, Trumark, CastleRock): Announced a deal to take United Homes Group private in a $221 million transaction, aiming to increase its U.S. presence. Daiwa wants 10,000 closings by year end. I’m not sure they’ll get that which is moot – the fact that they’ve put a number on the map is material.

- Sekisui House: Following its $4.9 billion acquisition of M.D.C. Holdings (Richmond American Homes) in early 2024, Sekisui is restructuring its U.S. subsidiaries – including Woodside, Holt, and Chesmar – under a unified structure that potentially creates a coast-to-coast monster.

Pay attention.

Japanese companies understand the long-term game better than anybody on the planet, bring deep pockets and a view that laughs in the face of quarterly earnings games.

The US housing market just got a whole lot more interesting and houses potentially just got a lot better built. Imagine living in a house made with Toyota quality.

I’m thinking US homebuilders like Pulte and DR Horton could be facing competitors they hadn’t counted on.

Hmmm. 🤔

5 – Dividends: why 8% can cost you 80%

People often ask me “where to hide” during times of market stress.

Dividend paying stocks can be terrific because they tend to fall less, stabilize first and recover faster, particularly if you are reinvesting the entire time.

Imagine, for example, that you owned Zoom which exploded during Covid but fell by 80% in 2022 and paid no dividend. It took a while to stabilize, is still volatile, and investors who owned it are still recovering.

Contrast that with owning J&J which fell 5-10% if memory serves, has paid increasing dividends for 25+ years through thick and thin. By early 2026, total returns would be roughly 20-25% including divvies.

Where do you start?

Most investors will chase yield but what they don’t understand is that’s a risky proposition because high yields aren’t always what they’re cracked up to be. In fact, high dividends tend to signal financial stress lurking like a great white shark where you can’t see it until too late.

I prefer stocks with positive TSY (True Shareholder Yield) because my research shows they tend to perform 10-15% better during market recoveries while also reducing risk simultaneously.

The One Bar Ahead® Family has this covered, and many of the choices in the Model Portfolio are performing as expected.

Hopefully you do too.

If not, please don’t delay.

The Iranian situation could get worse before it gets better so – I submit – it’s smart to make sure you have your bases covered.

Bottom Line

It never feels like a good time to invest, but history shows that it almost always is.

You got this – I promise!

You got this – I promise!

Now and as always, let’s MAKE it a great week and start the week strong.

Keith 😀