☕️ 💡Over-allocating to “safe” investments is one of the riskiest choices of all

Sep 22, 2025Howdy! 👋

Looks like the volatility I was concerned about last week may have reared its head, at least in the early going.

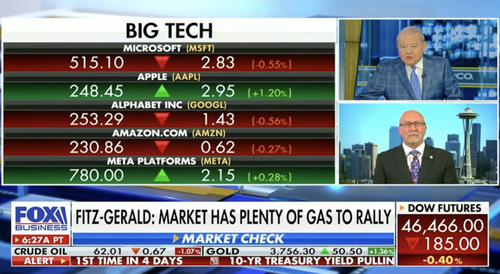

The path of least resistance remains higher and, for reasons I laid out in last night’s Sunday Short, I think it’ll be big caps that take the lead again fairly quickly. (Watch)

The super-savvy Stuart Varney also asked me about that as well as Apple earlier this morning; I hope you find my POV helpful. (Watch)

It’s what he asked next that matters most.

Many investors are scared outta their minds at the moment and with $7 trillion on the sidelines, “what’s wrong” with keeping that money in money market funds if retirees don’t want to take the risk.

In short, nothing.

If they understand the tradeoff.

Over allocating to “safe” investments is one of the riskiest choices of all.

Let me explain.

There are 5 big things to think about.

1 – Longevity risk

The average 70-year-old has a 1 in 5 chance of living to 95 and a 1 in 10 chance of living to 100. That means your portfolio may need to last another 30 years or even more.

A money market may feel good, but 4% simply isn’t going to keep up with lifestyle needs, living expenses and medical inflation.

Simple as that.

2 – Inflation risk

People are breathing easier with inflation coming down but that’s a mistake. Just 3% inflation can cut your purchasing power in half in 24 years or less.

Most investors do not understand how this works against ‘em.

Respectfully, I submit that inflation is far more dangerous than market volatility.

The markets have a very defined upside bias over time and that works in your favor but, to a point I make often, only if you’re in to win.

3 – Spending isn’t “just” about living

You and I work hard for our money and it’s logical to think that we’ve “earned” it when it comes to spending.

Here’s the challenge.

Retirees and those who are about to retire tend to be more frugal but still spend regularly which means that a portfolio locked into low returns will deplete faster than one that has a growth component all the way to sunset.

You don’t need to go crazy or do anything stupid, mind you.

Even a tiny amount invested in growth can radically change your experience, your outcome and your longevity when it comes to money.

People tell me they don’t have “time” frequently and I understand that.

Just $1,000 invested in Palantir a year ago would be worth $4,851.60 today.

Or IonQ… $8,530 today.

Heck, even the SPY – a popular ETF choice – would be $1,181.80 today.

The same $1,000 invested in a money market at 4% would be worth $1,040.

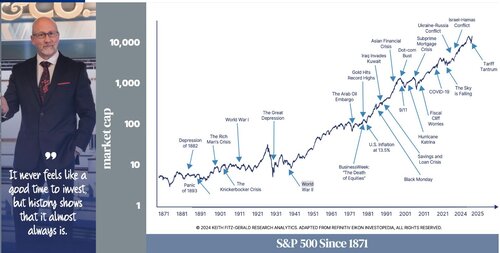

History suggests that there are 10-15 Palantirs and IonQs out there right now and investing even a tiny amount in ‘em can make a huge difference over time. Your job as an investor is to find ‘em and latch on. Mine is to help you do that if I can.

4 – Security and opportunity are not mutually exclusive

Many retirees think they’re protecting their wealth by being cautious but what they’re really doing is trying to protect short-term comfort at the expense of long-term solvency.

In other words, they feel great that they’re sidestepping perceived risk but what they’re not understanding is the opportunity cost associated with doing that.

You’re not alone if you’re feeling this way right now.

Every dollar parked in cash is a dollar that is not compounding and not growing. Even modest growth over a 10-, 15- or 20-year period can mean the difference between living the life of your dreams and scraping by.

Put another way, the choice isn’t the visible risks you perceive today but the invisible opportunity cost of tomorrow because the pain of temporary drawdowns today will pale in comparison to the pain of outliving your money.

5 – You can do BOTH

Wall Street has sold investors a bill of goods for decades.

It’s not an “either-or choice.”

You can still have plenty of safety for near-term cash needs while keeping a carefully planned growth sleeve, income and the like invested for the long-term.

There are all kinds of ways to handle this.

Dividends, growth stocks with dividends, covered calls and more – all of which can create income streams while helping mitigate the fear of a downturn.

The real risk couldn’t be “realer” if that makes sense.

It’s not volatility like many think, but waking up at 85 and realizing you haven’t got enough money for the next 15 years.

The way I see it, you don’t just need your money now.

Investing – done properly – is about now, later and much, much later.

When I first began my career, it was commonplace to plan for a life expectancy of 85. Now, I think 95 is absolutely appropriate… which gives a lot of folks pause.

What’s more, you can’t let up like you’d think even though that’s accepted as dogma and taught as gospel to legions of financial planners.

We live in a world where technology is changing exponentially and that means investing differently with an eye on what the world will look like.

Not the one we knew.

I know that sounds scary but it’s not when you really think about it.

The very same technology will eliminate costs that presently concern us.

You don’t buy cassettes anymore, do you?

Imagine what happens when AI helps solve Parkinson's, dementia, cancer etc. Suddenly end of life care costs decline by an order of magnitude, potentially more.

And that, in turn, means quality of life goes up even as the “costs” decrease. I can easily envision health care costs finally coming down out of nosebleed territory, for instance.

And I expect Apple to play a key role in making that happen.

Here’s an example that’ll hit home.

Take your smartphone.

If you were to buy everything needed for the GPS it has on board in 1980s, a GPS system would have set you back $150,000, an accelerometer weighed 50 pounds and the tech that made it work set you back $1,000,000 or more.

Now you can get all of those things and more for a coupla bucks. Maybe even for free depending on your mobile carrier.

The iphone and all the goodies on it fit in your pocket.

BTW, if you’ve found today’s 5 with Fitz helpful, you might enjoy One Bar Ahead® just like other like-minded folks who tell me it’s changed their lives. (Learn more)

If you’re covered, fabulous!!! 😀

Bottom Line

Fear is a powerful anti-motivator, yet one of the single biggest and most compelling investing opportunities if you can overcome it.

As always, let’s MAKE it a great day and start the week strong!

You got this – I promise!

Keith 😀