☕️ Three companies to consider and one to avoid if peace breaks out

Apr 06, 2026Howdy! 👋

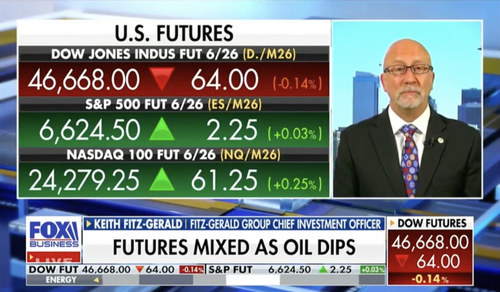

The markets are slightly up as I type on news that there may… just may… be a peace deal on the table between the United States and Iran.

I won’t hold my breath but here’s to hoping news reports are accurate.

You?

This market will be gone like a rocket if there is a peace deal which is why the smartest move you can make right now is to prepare for that eventuality.

At the risk of sounding like a broken record…

Investing in optimism beats cowering in pessimism any day… every day.

Here's my playbook.

1 – Three companies to consider and one to avoid if peace breaks out

Peace on deck or more fighting?

Regardless, tough markets make investors do silly things.

Like sell off some of the world’s best stocks.

That’s why the super savvy Ashley Webster asked me which companies I’m watching this morning and if I’d consider buying under the circumstances. (Watch)

Definitely.

2 – When Jamie Dimon writes, smart investors read

JPMorgan CEO Jamie Dimon's annual letter dropped this morning — all 48 pages of it — and it's worth your time.

CNBC reports that Dimon flags geopolitics, AI uncertainty, and private market risks as his top concerns while at the same time striking a note of resilience. With America celebrating its 250th anniversary, Dimon called this the perfect moment to rededicate ourselves to the values that built this nation — freedom, liberty, and opportunity. (Read)

I agree wholeheartedly.

My take has always been — and will continue to be — that this country is filled with resilient, remarkable, and clever people who rise to the occasion when needed. While it’s true that the path forward may not be smooth or straight, it IS very much still there.

I look forward to Dimon’s letter every year and, in fact, consider it “must read” material.

This year I expected Dimon to paint a broadly constructive picture of the US economy heading into 2026, citing the tailwinds from tax cuts, a deregulatory agenda, and AI-driven productivity gains – and he did. At the same time, I also expected him to clearly articulate the world as he sees it – and he did that too.

Dimon doesn’t sugarcoat risks, which is one of the things I like about him and have for years.

In fact, I share his perspective on many of ‘em including inflation … what he calls the “skunk at the party" — especially if the Iran war keeps oil elevated and supply chains scrambled. (Read)

Dimon is an exceptionally gifted thinker.

Whether you agree with every word that comes out of his mouth or not, I encourage you to carve out time to read what he has to say. Especially if you’re an investor.

Why?

Because great CEOs tend to run great companies and put up great results over time – which is why I place a priority on evaluating executives as part of the investing process. Many, like Tesla CEO Elon Musk, are incredibly controversial but that doesn’t change the picture.

JPM’s stock has returned roughly 152.9% since I brought it to the One Bar Ahead® Family’s attention on 3/7/22 versus ~54% from the SPY, a popular ETF choice for many investors. That's enough to turn every $1,000 invested into $2,529 today versus just $1,540 if invested in the SPY… a 1.64 to 1 performance advantage.

You know what to do.

Keith's Investing Tip: JPM is a textbook case of Buy the Best, Ignore the Rest®. The path to profits isn’t owning tiny slices of everything but meaningful chunks of the best companies. I hope you own it — and if you don't, I'd encourage you to reconsider.

Oh, and if you’d like some help or to become an OBAer – meaning a member of the One Bar Ahead® Family – you can learn more here.

3 – Coke: Why the dip isn't a buying opportunity

Coca-Cola just launched its first-ever ad campaign featuring multiple restaurant partners at once — 13 chains sharing the spotlight, all ending their order with the same three words: "And a Coke." Arby's, Domino's, Wingstop, Wendy's, Five Guys and eight others. (Read)

Thing is… the chains didn't pay a dime to be in it.

Smart move, but read between the lines.

Restaurant traffic fell 2% in February alone. Nearly 4 in 10 consumers said they spent less at restaurants in Q1 2026.

My experience is that when your customers' customers stop showing up, you feel it fast — and Coke gets roughly half its total sales from away-from-home channels: restaurants, theaters, stadiums. If food service sneezes, Coke catches a cold and the company’s own president John Murphy said as much.

We used to evaluate shopping mall investments back in the day based on parking lot counts so the thinking is similar.

I like that Coke is playing offense rather than waiting around but “liking” a company and owning a stock are two very different things which is why I cringe every time somebody asks if I “like” this stock or that one.

If you're into fizz (and divvies), seems to me that Pepsi's the better bet right now — diversified portfolio, stronger global growth, and a 3.62% yield that edges out Coke's 2.69%.

At the end of the day, Coke's ad campaign is clever marketing. My problem with it is that clever marketing doesn't fix a structural revenue problem when half your business depends on people eating out — and they're increasingly not.

Coke is a “prove it” stock at this point – meaning that the company needs to prove it can hold its away-from-home revenue before stepping in. There are better places to put your money right now… starting with Pepsi imho.

Keith's Investing Tip: A great brand and a great investment aren't the same thing — and confusing the two is one of the most expensive mistakes you can make as an investor.

4 – BlackRock just pulled a Walmart

BlackRock just filed to launch the iShares Nasdaq 100 ETF — ticker IQQ — going head to head with Invesco's QQQ, which has quietly sat on its golden throne for decades collecting its ~0.20% expense ratio like a toll booth nobody ever thought to go around. (Read)

Let's be honest about what's really happening here.

QQQ pulls in roughly $670 million a year in fees — effectively acting as an annuity Invesco has been cashing for 25 years while doing approximately nothing to earn it.

Here's the fee scorecard so you can appreciate just how cold-blooded this is:

- QQQ — 0.18%

- QQQM (Invesco's own cheaper version, because even they got embarrassed) — 0.15%

- IQQ (projected) — 0.12%… possibly 0.10% if BlackRock really wants to twist the knife

Six basis points sound like nothing but don’t make that mistake.

This is a VERY significant development.

There's over $440 billion tracking the QQQs so six “bips” – Wall Street speak for basis points – works out to roughly $260 million a year just on the fee difference alone.

Money that would flow straight back into your pocket potentially.

This is classic BlackRock.

Just like Walmart, they spot a fat, happy monopoly sitting on a pile of fee revenue, show up with a lower expense ratio, weaponize their $14 trillion in scale, and wait.

They did it to State Street, across fixed income and with IBIT in the Bitcoin ETF space — and dominated inflows within months of launch. Invesco just became the next name on that list.

You can almost hear Larry Fink saying "nice little ETF you've got there.” while trying not to drool.

Why it matters: QQQ's only real moat has always been liquidity and habit. Advisors use it because everybody uses it. That's the entire thesis. The moment IQQ launches at 0.12% — or lower — and BlackRock floods it with institutional seed money and its iShares distribution machine, that moat starts looking more like a puddle imho. Watch the final fee announcement closely… if it comes in at 0.10%, this isn't a fee war — it's game over for Invesco.

What to do: Sit back and let them fight. A fee war on one of the most popular trades on the planet is unambiguously good news for investors who own the QQQs.

Keith's Investing Tip: The best thing that can happen to a monopoly's customers is competition. The worst thing that can happen to the monopoly is BlackRock filing an SEC registration statement to enter the game. YOU can win either way.

5 – Calling all OBAers – two new recommendations in the April issue

Just in case you missed it over the Easter weekend, the April issue of One Bar Ahead® dropped on Friday.

Enjoy!

Bottom Line

World class companies get beaten down more often than you’d think for reasons that have nothing to do whatsoever with the business case for owning ‘em. So, not surprisingly, it stands to reason that you’ve often got one heckuvan opportunity when you can identify one of ‘em.

You got this – I promise!

Now and as always, let's MAKE it a great day and start the week strong.

Keith 😀

PS: Thanks to everyone who took a moment to chime in on my formatting experiment last week! And, of course, stay tuned – thanks for your help 😊