☕ Two stocks for better AND for worse

Mar 16, 2026Howdy! 👋

It’s nice to have some green on the screen this morning in the early going.

That said and at the risk of being a party pooper.

I’m not convinced that the markets are anywhere close to being outta the proverbial woods yet for reasons that I’ll explain in a moment.

I want you to think about something.

Quiet resilience.

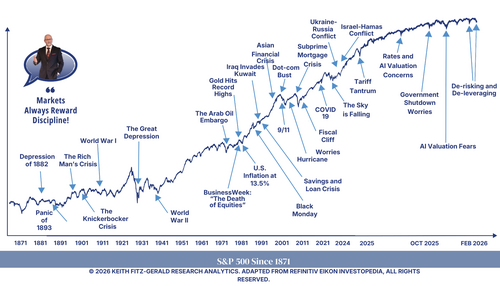

Running for Treasuries sounds smart and safe but trading in 4% for 20% - 70% may not be. The average recovery for all 10 major conflicts over the past 35 years has been 27%.

History shows very clearly that fully invested portfolios outperform attempts at timing.

What people don’t grasp.

The "best" days inevitably tend to cluster right after the worst ones— in other words, sell during the dip, and you lock in the losses while sitting out the rebound. Then you’ve got to get back “in” which is another can of worms all its own.

My research - and that from people a whole lot smarter than I am - shows that missing just the 10 best market days over 20 years can cut returns in half (from ~9-10% annualized to ~5-6%), and missing the best 20 days often slashes them by 70% or more.

I don’t know of too many investors who can give up that kind of profit potential but they try anyway with predictable results.

Staying invested and buying more is exactly what you want to do if you can.

Be in to win or you won’t… win!

Here’s my playbook.

Two stocks for better AND for worse

The super-sharp Stuart Varney kindly invited me back again this morning and had a timely question ‘Why do you think things could get worse before they get better?’ And, of course, which stocks could be smart choices for savvy investors.

I loved both questions frankly.

Too many people are still chasing “hot” stocks, a monster mistake in my book.

Buying great companies that’ll be there when you need ‘em, kick off huge dividends and provide “must have” products and services never goes outta style especially when the markets get spicy. (Watch)

Now a special look at an important question I’m getting a lot at the moment.

…“What do you tell older investors who can’t afford losses right now?”

Three things.

First, do NOT panic.

Selling low during a dip locks in losses AND makes it harder to recover when the markets bounce back… and they will. Despite oil shocks, war, recessions, Fed follies and more.

Your long-term plan was built for ups and downs.

And you do have one, yes?

If not, you know where to find me.

Second, build or build up your “safe bucket.”

All investments involve risk, and there’s no getting around that. If you can’t stomach the thought of losses, then you have no business being in the markets.

Simple as that.

But that doesn’t really answer the question.

I’ve always encouraged investors to have at least 2-5 years set aside in what I call the “Safety Bucket” – meaning ultrasafe things like cash, high-yield savings accounts, Treasuries and so on.

The fabulous Suze Orman shares my perspective and routinely encourages investors to invest ONLY the money they won’t need for at least 5 years. And she knows a thing or two about money! 😀

Having a “Safety Bucket” is a buffer against unexpected market turbulence.

That way you can live your life without having to sell at a loss while you wait for the markets to regain their footing.

If you don’t have your own version of a “Safety Bucket” – then I cannot say this strongly enough – start one now without delay. Set aside cash and/or shift from stocks and longer-term bonds as part of a conscious rebalancing effort if needed.

Doing so protects against what’s called “sequence of returns risk” – a $5 way of saying that you’ve allowed yourself to get into such a position that a few bad years or even months permanently dents your portfolio.

And third, reassess your allocation – meaning how much of what you own where

Consider dialing back your portfolio to the point where you can sleep peacefully at night.

Many folks have enjoyed huge runs in companies like Palantir, for example. Even after all the selling it’s returned ~1,505% since it went public. The S&P 500 over the same time frame has returned ~99%.

Doing a little profit harvesting could be just the ticket.

People ask me about specific percentages all the time – as in how much should I sell or keep in cash - but it really IS no more complicated than regaining peace of mind… whatever that number happens to be.

You can also consider leaning on guaranteed income sources like Social Security (even delaying claiming if possible for higher monthly checks). If you’ve got a pension, great… you’ve got a foundation.

Ruthlessly re-evaluate your budget and consider delaying big purchases which buys you time for the markets to stabilize.

Your goal right now isn’t to get rich – it’s to not go broke.

Keith’s Investing Tip: History shows two things: a) bottoming is a process and b) recoveries tend to start when fear is highest.

Bottom Line

You really do got this – I promise!

Focus on what you can control and give yourself some leeway for feeling uneasy for the simple reason that you’re not alone.

I will be with you every step of the way!

Now and as always, let’s MAKE it a great day.

Keith 😄