☕️ Two stocks I’ll be buying if markets give me the chance

Dec 29, 2025Howdy! 👋

Welcome back to another holiday-shortened week!

I had hoped that we’d see a final push higher this morning to crest 7,000, but that looks not to be the case. Instead, all three indices are taking a breather this morning while the go-fast crowd takes profits.

To paraphrase a line in the 2006 rom-com A Good Year, it’s greedy bast**ds day.

Stay focused.

One down day does not make a trend.

Besides and not for nothing…

History is very clear.

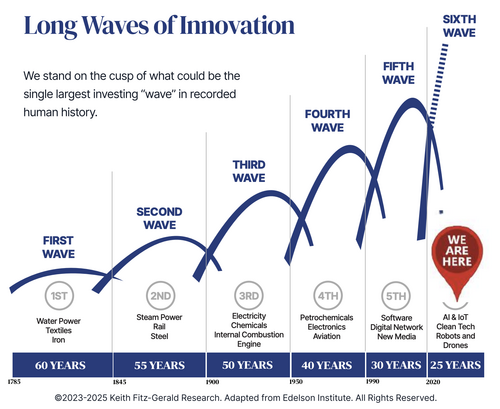

Nearly any short-term market reaction is a reason for long-term investors to buy… especially when it comes to companies making long-term growth possible.

Here’s my playbook.

1 – Two stocks I’ll be buying today if I get the chance

And, where do the markets go from here?

I sat down this morning with the venerable Ashley Webster who asked me specifically for my take ahead of this morning’s opening bell. (Watch)

2 – Why silver (and gold) are riskier than most investors think

The myth is alive and well lately.

Silver is really an industrial metal in “need” for everything from production to AI.

Prices just hit $80 for the first time and now - ta da - they’re dropping sharply in early going leaving a new group of folks chasing fairy tales high and dry.

The real “trade” is understanding what silver is warning you about.

Hint it’s not “utility.”

But leverage.

Trade Idea: A bear put spread – meaning buy the $65put and sell the $40 put at the same time – a move that caps max profit potential buy slashes cost and risk. Or, longer dated LEAPs puts to give this trade some breathing room without getting crushed by time decay (theta).

Hmmm.

3 – Should you buy Intel because Unka Jensen is?

Team Jensen just quietly followed through on a $5 billion Intel investment. (Read)

So the logical question I get from a lot of folks who want to do the same thing is do you “like” Intel stock?

Nope.

Odds are, neither does Unka Jensen. He’s simply buying another path to profits.

I’d rather own Nvidia directly.

It may not be perfect, but it works for me.

Keith’s Investing Tip: Think like a shark (Nvidia) not like a minnow (Intel).

4 – Owning the plumbing isn’t the same as owning the profits

SoftBank is buying DigitalBridge for about $4 billion, adding data centers, fiber networks, towers and edge infrastructure to its portfolio. (Read)

How practical.

You see, DigitalBridge owns the kind of assets nobody talks about until they become scarce — the pipes, wires and facilities that digital growth depends on. So if you believe computing demand keeps rising, like I do and Masayoshi Son apparently does, owning the infrastructure underneath it makes sense.

The challenge is that infrastructure always comes with trade-offs.

For one thing, it’s expensive to build, slow to adjust and heavily influenced by interest rates, regulators and governments. You don’t get many second chances if the timing is off.

My preference hasn’t changed.

I’d still rather own the companies designing the critical hardware and systems that sit inside that infrastructure because those things tend to have more flexibility, better margins and far fewer moving parts. Not to mention considerably bigger profit potential imho.

You know what to do. But if you don’t and would like some help, I'll be here.

5 – GM’s dividend looks nice, until you do the math

CNBC reports that GM stock is having its best year since 2009… when it emerged from bankruptcy, something a lot of folks have forgotten about. (Read)

How much “best?”

Try +55% this year - on top of 5 consecutive months of higher prices that beats Tesla, Ford, Honda, and a host of others.

The real question is can the gains continue.

Barra says that “Great vehicles, innovative technology, a rewarding customer experience, along with strong financial results, will continue to set GM apart in an increasingly competitive landscape” and I don’t disagree.

However, I am hard pressed to see where this goes from here.

Seems to me that GM stock is enjoying a great run based on a relaxed regulatory environment rather than seriously impressive cars or breakthrough tech.

If you’re a dividend investor maybe.

The company’s yield is 0.97% but has grown at 13.37% over the past decade which is great.

What I can’t get past is that the True Shareholder Yield (TSY) is -3.65% which means that it’s costing you money as a shareholder rather than returning it to you. And I don’t like that.

My research shows that companies with positive TSY tend to be far better investments over time. Specifically, companies with positive TSY (True Shareholder Yield) grew at roughly ~10-12.5% a year while those with negative TSY grew by less than 4%... ~9% difference.

That’s the difference between $25,937 and $14,802 on every $10,000 invested over 10 years. Or $259,374 and $148,024 on every $100,000 invested over the same time frame.

I don’t know of too many investors who can throw away that kind of potential.

If you can, good on you. 💯

If not and what I am describing has piqued your interest because more profit potential and better income over time is something that makes sense, I’ll be here.

Bottom Line

People playing for pennies at moments in time usually lose out to those playing for dollars over time. 💡

As always, let’s MAKE it a great day and start the week strong.

Then, finish the year strong!

You got this – I promise!

Keith 😀