☕ Santa pop or humbug drop?

Dec 01, 2025Howdy! 👋

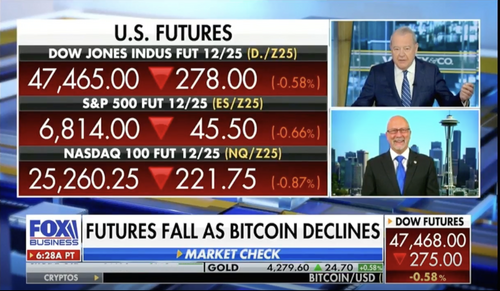

I had hoped that the markets would catch a bid – meaning run higher – out of the gate when I recorded Sunday’s short (and futures markets were still closed so I had no way of telling which way the wind was blowing). (Watch)

Clearly the markets have other ideas.

Normally, I’d look to Treasuries as a “tell” – a poker expression meaning a subtle clue that reveals what’s really going on – but in this case it’s bitcoin which is getting pasted again.

Predictably, scores of folks who thought they were investors are finding out the hard way that they’re speculators but that’s a story for another day.

What you need to recognize is very simple.

There are still more net sellers than buyers this morning which is why flows are negative; the tide is simply going out.

Frustrating perhaps, but not the end of the world either.

We’ve been here plenty of times.

Today’s market action reinforces something we talk about regularly… the need to focus on what you can control rather than worrying about the stuff you can’t.

And what might that be?

I’m glad you asked:

… buying great companies

… lining up your money with unstoppable themes based on where the world is going, not where it’s been

… using tactics that help control risk every step of the way

And that, mind you, is just for starters!

I wouldn’t be surprised, btw, to see today’s market reverse higher by close.

No guarantees but just pointing out the obvious.

It’s only a matter of time.

Here’s my playbook.

1 – Santa Pop or Humbug Drop?

I sat down with the super smart Stuart Varney ahead of today’s opening bell and he wanted my thoughts on whether we’re more likely to see a Santa Pop or a Humbug Drop. And you just know I’ve got a few thoughts on that one! 😎 (Watch)

We also spent a minute on some of the big earnings rolling out later this week… including one stock I’ll be avoiding entirely, one that I believe is at the very head of the class, and another that’ll give us more useful information than any government statistics ever could imho.

2 – Breaking: Morgan Stanley finally reads the room

Morgan Stanley analyst Joseph Moore says Nvidia could rise to $250. (Read)

Umm, yeah. 🤔

Morgan Stanley announced substantially higher targets, saying that broad-based AI demand remains extremely strong, Nvidia is still dominating market share and supply remains tight into the future.

Gee, where have we heard that before?

Oh, right… you and I have been discussing those very talking points for several years.

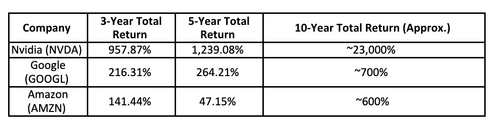

Since 2023 lows, in fact.

Nvidia has returned 1,118.08% since then while the SPY, a very popular ETF for many, has returned 84.67% by comparison.

MyPOV: Many investors want to be “right” about the stocks they own, but the world’s most profitable investors go to great lengths to be “profitable” even if they’re wrong.

Btw, my 12-24 month target is a skosh higher and that’s something the OBA Family knows all about. If you’d like to join ‘em and learn more about how that kind of perspective can make a huge difference in your investing success over time, I’ll be here.

Or you can wait until another of Wall Street’s analysts steps up after having missed a massive portion of the move higher. 🤦

Keith’s Investing Tip: Wall Street’s sell side analysts are often notoriously late to the party more because their models don’t tend to update until after the big moves are evident to dang near everyone. Not surprisingly, it’s almost always more profitable over the long term to invest based on where the “puck is going” not where the consensus finally notices it went.

3 – Lilly to Novo: catch me if you can!

Eli Lilly just dropped cash prices on its Zepbound weight-loss vials to as low as $299 a month on LillyDirect. (Read)

Novo Nordisk, meanwhile, has been scrambling to match with its own price cuts.

You’ve heard me say before that Lilly has the upper hand in this space and, not surprisingly, what’s happening reinforces that view.

CNBC notes that the lower prices come ahead of broader federal agreements taking effect in January — deals that will make GLP-1 drugs easier for Americans to access and afford.

What’s more, Lilly is moving ahead on discounts before its multi-dose pen gets FDA approval, which reinforces my contention that the company is playing offence while everyone else is playing catch-up.

I think there’s a case demand hits another gear in the next 12-24 months (even though it was arguably off the charts).

Last week I suggested Deep In the Money calls as one possible way to get on board and I still think those are a viable choice despite today’s slide. Buying a few shares could work too but I want to see more “value” for my money first.

Hmmm. 🤔

Keith’s Investing Tip: Investing is a series of choices which is why you’ve got to constantly weigh alternatives against each other. For example, I’d love to own Eli Lilly but have got to balance that against two other choices I already own and recommend to the OBA Family that (for now) still have considerably broader and more defined upside. “Collecting” stocks is never a good idea because it reduces your profit potential. Focus, on the other hand, helps you win. So, focus!

4 – Three things that give me pause about Airbus

Airbus shares dropped nearly 10% after the company disclosed yet another problem with its A320 family — this time a new industrial quality issue involving fuselage panels on dozens of jets. (Read)

And the timing couldn’t be worse.

This comes right after the massive software glitch that grounded more than half of the global A320 fleet over the weekend — one of the largest directives in Airbus’s 55-year history. The disruption stretched from the U.S. holiday rush to Australia and hit airlines and suppliers alike.

Quality issues… software failures… delayed deliveries. It’s all starting to pile up in ways that are getting harder to ignore.

Three things jump out at me.

First, when you see back-to-back failures on this scale — mechanical and digital — it usually points to deeper process problems, not isolated bad luck.

Second, Airbus is already behind on production targets. Any quality issue that slows deliveries only widens the gap with Boeing at a moment when global demand for narrow-body aircraft is surging.

Third, the market reaction tells you everything you need to know. A drop this sharp means investors are questioning management’s grip on manufacturing, oversight, and operational discipline.

Aviation is unforgiving, and rarely wobbles alone.

Meanwhile, I’ve got my eyes on a Chinese maker moving into global markets. Shares are not yet traded in the West doggonit! 👀

5 – “Keep your friends close but your enemies closer”.

AWS and Google Cloud just shocked the tech world by teaming up. (Read)

Cuz, you know.

Sworn rivals suddenly holding hands is totally normal. 🙄

Wall Street is already trying to spin this as some sort of grand “innovation moment.”

I say look at what’s actually happening here.

Both companies finally realized what customers have been screaming for years… multicloud networking is a mess.

Connecting AWS to Google Cloud traditionally meant long waits, hardware headaches, and enough networking config to make a grown engineer cry.

We’ve run into that very issue many times over in my own companies and to say it’s a pain in the you know what is a massive understatement.

Integrating AWS with anything is a massive, often brain-damaging undertaking. And our experience with Google’s cloud much the same. So much so that we’re working with Azure because “most” of what we want to do we can do inside a single walled garden.

But I digress.

AWS and Google have announced a jointly engineered solution that supposedly lets customers click a button and create private, high-speed connectivity between clouds in minutes.

I’ll believe it when I see it.

Customers hold the cards — not the cloud providers.

That’s the real headline, or at least should be.

Look closer and you’ll see the tell… both companies are “open standards,” “interoperability,” and “cross-cloud architecture.” Code for “hey, the risks our customers walk is higher by the minute.”

Data is like money which, in turn, is a lot like water.

Repeat after me.

Money and data will both flow to where they’re treated best.

Invest accordingly.

Google and Amazon are both in far deeper trouble than most investors recognize, imho.

And yeh, I know… some folks may be thinking Keith’s “wrong” about Google again.

I get that a lot lately.

Google’s in the news and short-term returns have been fantastic – no doubt about it.

Respectfully and to the point I made in #3 today, investing is about choices and perspective. And I choose to own Nvidia over both Google and Amazon because I have a longer term, much more zoomed out perspective.

But, hey, it’s a free country – if you want to own Google or Amazon, knock yourself out! 😄

Source: Koyfin, as of 1st December 2025 at time of typing.

Bottom Line

Your mindset can make or break your investment journey.

Cultivate optimism, stay positive, and believe in YOUR ability to create wealth.

Learn, ask questions.

MAKE it happen.

You got this – I promise! 💯

Keith 😀