☕️ United Health: Buy, Sell or Hold?

Jul 16, 2026Howdy! 👋

The S&P 500 and the snazzy nazzy are both red, while the Dow is green in early trading.

The official story being bandied about as I scan the headlines is that there’s a classic sector “rotation” out of semiconductors and AI-related stocks.

Not.

Rotation implies that the markets are a zero-sum game because investors move their money from one sector to another. If money comes out of tech, it must therefore go into value, or dividends, or bonds or something else according to pundits. Then back again.

That’s not how the game is played.

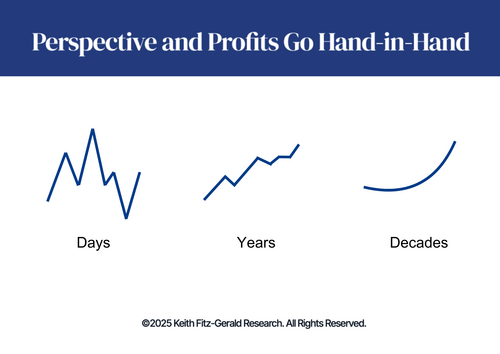

The markets continually create new profits and attract new money as prices rise and fall which is why history clearly shows that long-term investing gains overshadow short-term trading results over time.

Case in point.

If you're thinking about the next 24 hours, the odds of a higher close are barely better than a coin flip. If you're willing to give it 3-5 years, the odds jump into the 80% range. Give it a decade, and you're looking at a number north of 90%. Two decades… now you’re talking 100%.

Folks tell me regularly that they don’t have that kind of “time” whenever I bring up stuff like this but what they don’t realize – or more likely refuse to acknowledge – is that doesn’t change the math. Just the clock you’re watching.

Keep it stupid simple.

A dollar invested today has the same expected long-run return whether you’re 35, 75 or even 105.

That’s a hard concept to grok – I get it.

Let me put it this way by asking a question.

Have you ever seen a long-term game at a Las Vegas casino?

Me neither.

Every casino game is engineered around short time horizons — spins, hands, rolls because the house edge needs quick decisions and small samples to work.

Markets run the other way.

The longer you stay at the table, the more the odds shift toward you, your money and your ability to build real, sustainable wealth.

Here's my playbook.

1 – Eli Lilly just bought its next growth story

Eli Lilly is acquiring psychedelic drugmaker AtaiBeckley for $2.8 billion upfront, with up to $1 billion more tied to milestones. (Read)

The deal gives Lilly access to AtaiBeckley's lead drugs, a nasal spray currently in Phase 3 trials for treatment-resistant depression, along with other psychedelics in development.

So?

Treatment-resistant depression isn't rare. It affects tens of millions of people including a friend of mine a few years back who couldn’t leave the battlefield no matter how hard he tried and what treatment he received.

Honestly, the standard playbook hasn't changed in decades. If something new can actually help, that's not just a win for patients but for Lilly and people like John too.

This is Lilly doing what Lilly does best.

The company has already committed more than $10 billion upfront this year alone across eight acquisitions, deliberately going after later-stage, more expensive deals now that it's settled into its role as the most valuable healthcare company on the planet.

MyPOV: Here's what I think is really going on. Lilly's stock has been almost entirely a weight-loss story for the last couple years, and a phenomenal one at that. But smart companies don't build their entire future on one drug class, no matter how good it is. This deal buys Lilly a second, completely uncorrelated growth story. Possibly a third, too.

It also doesn't hurt that the current administration has made psychedelic-based mental health treatment a stated priority.

Keith’s Investing Tip: When regulatory tailwinds and genuine unmet medical needs line up like this, that's usually an interesting sign for smart investors.

2 – UnitedHealth beat the Street again – buy, sell or hold?

UnitedHealth Group reported this morning, and the numbers were decent. (Read)

- Adjusted EPS came in at $6.38 vs. $4.90 expected — a big beat

- Revenue hit $112.03 billion vs. $110.85 billion expected

- Medical benefit ratio: 86.7% vs. 88.5% expected — the better this number, the more profitable the insurer

- Full-year earnings outlook raised to $19.50–$20 per share, up from more than $18.25

Two quarters in a row now the company has put up strong numbers.

I warned you to steer clear of UNH back in April 2025 for several reasons including a CEO bailing for "personal reasons," the first earnings miss since 2008, the Medicare Advantage margin squeeze, and the federal billing fraud investigation.

All of it played out exactly as advertised - shares dropped hard in the aftermath.

Now, two good quarters back-to-back is real progress, but even UnitedHealth calls this a 'multi-year journey,' not a finished turnaround. Shares are up ~74% from a $255.97 low earlier this year.

Time for a rethink?

Perhaps but here’s what I actually “think”…

Medical costs are still 'elevated over historical levels' by their own admission. Membership keeps shrinking too, with roughly 500,000 ACA exchange members and 1.1 million Medicare Advantage members expected to walk this year.

Then there's the DOJ investigation into Medicare billing which is still open. UnitedHealth says it remains 'supportive' of the probe, which strikes me as code speak for “hey, we’re putting on a bright smile for appearances.”

Trade idea: Putskies, short, or simply avoid until the stock can sustain $500 a share for a few quarters and earnings a few quarters more still. Better yet, just focus on buying the best and ignoring the rest. I think there are plenty of other companies out there with what I believe to be clearer, bigger profit potential and dramatically less baggage. Including Lilly, which I just mentioned and a handful of stocks that the One Bar Ahead® Family knows well. If you need help or would find some additional insight valuable, I’ll be here.

3 – Uber's $15 Billion answer to every 12 year old with a bike and a basket

Uber launched a $15 billion takeover bid for Delivery Hero, aiming to build the largest food-delivery platform outside China, spanning 99 countries. (Read)

Here we go again.

Freight. Grocery. Micromobility. Uber Ski. Now a food-delivery empire.

Uber’s reinvented itself more time than Facebook – err, Meta. Yet the core business remains… hauling humans and burritos from A to B.

MyPOV: Buying bigger isn't the same as buying better. True, Delivery Hero adds scale but it’s not a moat considering that any motivated 12-year-old with a bike and a basket can compete. Meanwhile, the real threat to Uber – autonomous rides and shipping with no driver at all – keeps getting closer. And not a peep from the C-Suite.

Keith’s Investing Tip: Management that won’t talk about “the threat” is telling you exactly how worried they are. Silence is not reassuring nor confident but a tell.

4 – Japan just launched the world's first national AI factory

Three guesses whose backing it and the first two don’t count.

Team Jensen, of course.

Nvidia is partnering with Noetra Corp. to build a Vera Rubin AI factory in Japan, packing 13,750 Vera CPUs and 27,500 Rubin GPUs to deliver 140 megawatts of data center capacity. (Read)

Nvidia is calling it the world's first national AI infrastructure built specifically for physical AI. It's backed directly by Japan's Ministry of Economy, Trade and Industry, and it'll power the FRONTia Project, developing open AI models for robotics, digital twins, and intelligent manufacturing that domestic companies across the country will be able to build on.

The stakes here are bigger than one factory.

Japan wants more than 30% of the global AI robotics market by 2040. That's a $133 billion opportunity, and this AI factory is the infrastructure Japan's betting on to get there.

Sadly, Japan's been slow to compete in software and consumer tech for decades. In fact, you could argue that they’ve been booted from many markets that they helped create and once dominated.

This smells different.

Fanuc and Yaskawa are already world leaders in industrial robotics. Toyota, Honda, and Hitachi know how to integrate technology into real products at scale. The one thing Japan didn't have was the compute layer underneath it all.

I do have one big question though.

Having spent nearly 40 years in Japan as a husband, father, investor and consultant, I fear that Japan may have lost the ability to innovate. So – and this is tough to say because I love Japan – no matter how good the AI, the current crop of executives may not have what it takes to harness the one thing they need desperately to make this work… creativity and a willingness to put aside ridged hierarchy and long established social norms to unleash it.

Hmmm. 🤔

5 – TSMC adds $100B to US spending plan

It’s hard not to pick my jaw up off the floor.

Profits have blown by estimates again and yes, it’s raising capital spending again. (Read)

TSMC, in case you’re not putting the bits together – pun absolutely intended – is Nvidia’s primary chip supplier and the dang company now expects capital expenditures of $60 billion to $64 billion in 2026, at least $4 billion above its previous forecast.

What catches my attention is that the company also raised its revenue growth projection to slightly more than 40%, gobs above the 30%-plus increase it had previously anticipated.

I’d still rather own Nvidia because I believe it’s the better choice and higher in the proverbial food chain, but this is getting hard to ignore.

The question in my mind is tactics.

LEAPS, just for the heck of it? 🤷

I could also make the argument that a LowBall in the $375 range is attractive given all the bubble babble and volatility lately.

Bottom Line

Companies that hesitate become footnotes but the ones that lead become empires.

Investors, too.

Play offense, even if you must think defensively to do it.

Now and as always, let's MAKE it a great day. 💯

You got this — I promise!

Keith 😀